How wealth is distributed will always be a contentious issue, especially as the Baby Boomers (those aged between their late 50’s and late 70’s) wealth has grown exponentially over the last 20 years, compared to the wealth of the younger generation.

With most UK property in the hands of the older generation, with its total value about to smash through the £8 trillion barrier (up from £3 trillion at the start of the Millennium), is it right that so much wealth is concentrated in the hands of the older generations?

As national house prices have continued to grow unabated (for example in the last eight years by 49.9%, whilst real take home pay has only increased by 11.8%), this has meant younger people are finding it even harder to get onto the property ladder and those already on it to move up it.

Looking at the older end of the age range for home ownership …

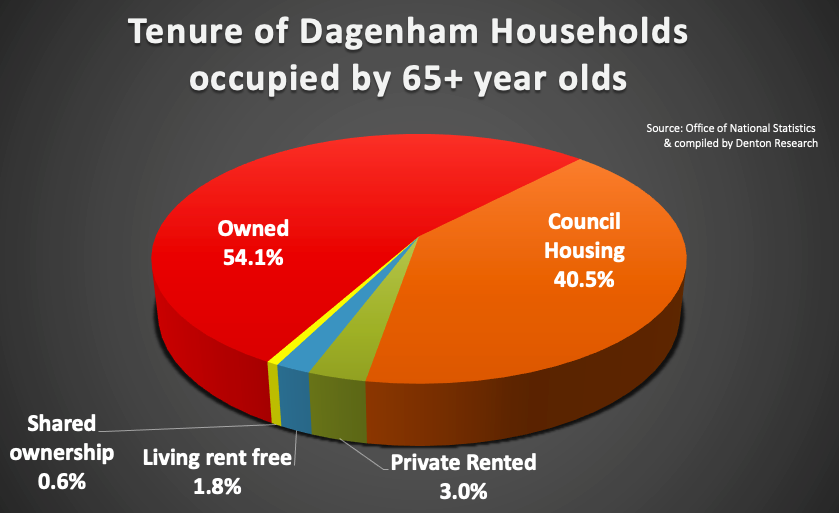

of the 43,247 homes in Dagenham, 8,672 households are 65 years or older and 54.1% of those households (4,690) are owned

(mostly without a mortgage)

With a full split as follows …

- Owned 54.1%

- Council house 40.5%

- Privately rented 3.0%

- Living rent free 1.8%

- Shared ownership 0.6%

I talk with many Dagenham pensioners who want to move yet are unable to. There appears to be a shortage of suitable properties in Dagenham for members of the older generation to downsize into. Due to their high demand and low supply, Dagenham bungalows and suitable ground floor apartments achieve on average a 15% to 25% premium per square foot over two/three storey properties. Yet would it surprise you only 1% of new builds in the UK are single storey bungalows (compared to 7% 25 years ago)?

Dagenham pensioner homeowners are now worth £1.65bn

YouGov did a survey a couple of years ago and they found that just over one third of homeowning pensioners in the UK were looking to downsize into a smaller property. As I have stated before, as a nation, we need to rethink how we can encourage older homeowners to sell their larger homes to release them to the younger families that desperately need them.

The Government over the last 11 years have appeared to target all their attention on first-time buyers with a strategy such as the Help to Buy Scheme. However, this doesn’t address the long-established under-supply of appropriate retirement housing vital to the needs of Dagenham’s quickly ageing population. Unfortunately, Dagenham’s housing stock is sadly ill-equipped for this demographic shift to ageing homeowners.

Also, to add insult to injury, those more mature Dagenham pensioners in their 80’s and 90’s who do live in the restricted number of Dagenham bungalows and suitable ground floor apartments are finding it difficult to live on their own, as they are unable to leave their bungalow/apartment because of a shortage of sheltered housing and ‘inexpensive’ care home places.

This in turn means the younger 60 to 70 year old Dagenham retirees (in their bigger two/three storey family houses) can’t buy those Dagenham bungalows (occupied by the older retirees), which means those Dagenham families in their 30’s and 40’s can’t buy those larger family houses (occupied by the younger 60 to 70 year old retirees) they need for their growing families … it’s like everyone is waiting for everyone because of the logjam at the top of the property ladder.

So, what is the solution? Quite simple – build more homes!

In the last 30 years, the UK population has grown by around

12 million people, yet the number of properties has only grown

by around 4.2 million

With obstructive planning regulations, immigration, people living longer and increased divorce rates (meaning one family becomes two) we have needed 275,000 properties to be built a year since the Millennium to just stand still and meet demand. Twenty years ago, the UK was building on average 185,000 households a year, that figure dropped in the five years after the Global Financial Crisis in 2008 to 140,000 households a year. Thankfully that has increased steadily over the last five years and last year we created 245,000 households in the UK however, we still have all those years since the Millennium to make up for.

The answer is to build on more land for starter homes, bungalows and sheltered accommodation because land prices are holding back the property market, as the larger national building firms are more inclined to focus on traditional two and three storey houses and apartments than bungalows (because they make more money from them). You might say there is no land to build the property on, yet …

only 1.2% of the UK is built on with residential properties

So how could Dagenham people make money on this news? Shrewd Dagenham property investors should consider purchasing bungalows, especially ones that need some titivating (say after somebody has passed away possibly). Bungalows purchased at the right price and location are a great gamble for flipping. They should also be considered for renting out as demand will only outstrip supply. This would be a start to the solution of rebalancing the Dagenham property market so everyone is happier with their lot.

If you would like a chat about the Dagenham property market – don’t hesitate to give me a call.